Investment property loan rates currently average 7-7.5% for 30-year fixed mortgages, which are roughly 0.5-1% higher than primary residence rates, but the advertised rate tells only part of the story. The loan type you choose, lender you work with, and how you qualify matter more than the rate itself when building a profitable short-term rental portfolio.

If you’ve ever found yourself wondering, “where do I find the lowest loan rates to finance my investment property?” This guide is for you. It breaks down today's lowest investment property rates across different loan products, explains exactly how to qualify for the best pricing, and shows you where to find lenders who actually understand short-term rental cash flow instead of discounting your Airbnb income by 50%.

Today's Lowest Investment Property Loan Rates

Investment property mortgage rates typically run 0.5% to 1% higher than primary residence rates, with current averages for 30-year fixed loans ranging from 7% to 7.5%. Lenders view rental properties as higher risk because borrowers prioritize their own home payment during financial hardship, leaving investment properties more vulnerable to default.

Your specific rate depends on several interconnected factors. Credit scores above 740 unlock the best pricing tiers, while down payments of 25% or more reduce lender risk and lower your rate. Debt-to-income ratios below 43%, substantial cash reserves (typically 6-12 months of operating expenses), and property type all influence the final number you'll see on your rate sheet.

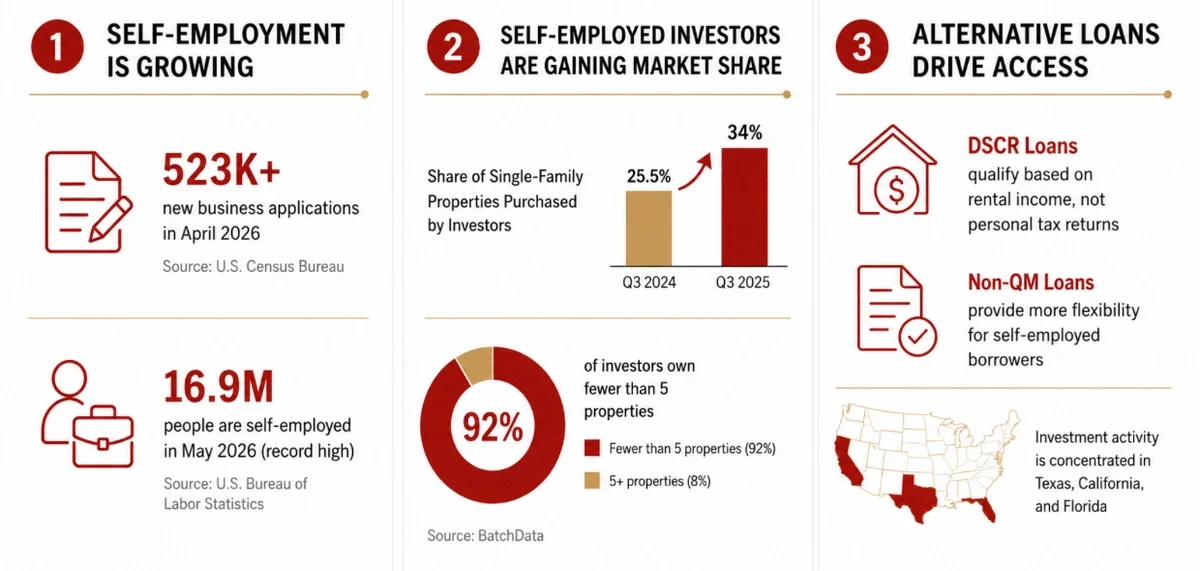

Here's what most investors miss: the lowest advertised rate rarely translates to the best deal for your situation. A conventional loan at 6.75% might require 30% down and extensive income documentation that disqualifies self-employed investors, while a DSCR loan at 7.25% with 20% down and no income verification closes in half the time and enables portfolio scaling.

The rate that works best combines competitive pricing with terms you can actually meet. Properties with verified income history strengthen your rate negotiations because lenders offer better terms when you present historical cash flow data rather than projections alone.

Find a Lender that Specializes in Short-Term Rentals

Connect with lenders who actually understand short-term rental cash flow and offer DSCR loans, portfolio financing, and investor-friendly terms.

Get Matched with STR LendersWhy Investment Mortgage Rates Run Higher Than Primary Home Loans

Lenders charge higher interest rates on investment properties because rental property loans carry more default risk. If tenants fail to pay or properties sit vacant, investors may struggle to cover mortgage payments—and during financial hardship, most borrowers protect their primary residence first.

This risk assessment translates directly to stricter qualification standards. Where primary residence loans might accept 3-5% down payments, investment properties typically require 15-25% minimum. Credit score requirements jump from 620 to 680 or higher, while cash reserve requirements increase from zero to six months of mortgage payments.

The regulatory framework reinforces the difference. Fannie Mae and Freddie Mac impose loan-level price adjustments on investment properties that increase costs by 1.5-3% of the loan amount depending on credit score and down payment. Lenders pass along the mandatory risk premiums through higher rates or upfront fees.

STR-specialized lenders often offer more competitive effective rates than conventional lenders for investment properties because they accurately assess short-term rental income potential rather than discounting it by 25-50% like traditional underwriters do.

Loan Types With the Cheapest Rates for Rental Properties

Different loan products serve different investor profiles, and the "cheapest" option depends on your financial situation and portfolio goals.

Conventional 30-Year Fixed

Conventional loans backed by Fannie Mae or Freddie Mac offer the lowest advertised rates, currently 6.5-7.25% for well-qualified borrowers. You'll need a 680+ credit score, 20-25% down payment, debt-to-income ratio below 43%, and two years of documented W-2 or tax return income.

The catch? Conventional loans cap most investors at 10 financed properties and severely discount or ignore short-term rental income potential. If you're self-employed or your STR generates $5,000 monthly but comparable long-term rentals only bring $2,000, conventional underwriting works against you.

DSCR Loans (Recommended for STR Investors)

DSCR (Debt Service Coverage Ratio) loans qualify you based on property income rather than personal income. Rates typically run 6.75-8.25% (slightly higher than conventional), but DSCR loans eliminate income documentation requirements and allow unlimited property scaling. These DSCR loans are what the lenders in Rabbu’s network specialize in underwriting.

The lender calculates monthly rental income divided by monthly debt obligations (mortgage, taxes, insurance, HOA). A DSCR of 1.25 means the property generates 25% more income than its debt service, demonstrating strong cash flow that justifies the loan.

For a property generating $4,800 monthly with $3,600 in debt obligations, your DSCR is 1.33, which is well above most lender minimums. Use Rabbu's Calculator to model DSCR ratios before making offers, ensuring you target properties that qualify for the best rates.

Why DSCR loans work for STR investors:

-

No personal income documentation required – your tax returns and W-2s are irrelevant

-

Portfolio scaling without limits – no 10-property cap like conventional loans

-

Faster closing timelines – 15-30 days vs. 45-60 for conventional financing

-

Self-employed friendly – business owners who minimize taxable income face no penalties

The slightly higher rate becomes less significant when you factor in the ability to close multiple deals per year instead of hitting qualification barriers after 2-3 properties.

Portfolio and Asset-Based Loans

Portfolio loans held by individual banks rather than sold to Fannie/Freddie offer customized underwriting outside standard guidelines. Rates vary widely from 6.5-8.5% depending on your relationship with the bank and overall portfolio strength.

Portfolio loans work well for unique properties that don't fit conventional boxes: rural cabins, non-warrantable condos, properties needing renovation, or investors with complex financial situations. The bank evaluates your entire relationship rather than checking standardized boxes.

Home Equity Loans and HELOCs

Tapping equity in existing properties to finance new acquisitions offers rates of 7-9% for fixed home equity loans or variable rates starting around 8% for HELOCs. This approach works when you have substantial equity but want to preserve conventional loan capacity.

The risk? You're leveraging your primary residence or existing rentals, increasing overall portfolio leverage. If the new property underperforms, you've put other assets at risk.

Don't Let Financing Kill Your Deal

Most banks don't understand short-term rentals. These lenders do.

Find a LenderHow to Qualify for the Best Investment Property Mortgage Rates

Securing the lowest rates requires strategic preparation across multiple financial dimensions.

Step 1. Boost Credit Score Above 740

Every 20-point credit score increase can lower your rate by 0.125-0.25%. The difference between a 680 score and 760 score might mean 7.5% vs. 7.0%, which translates to $60-80 monthly savings on a $300,000 loan, or $21,600-28,800 over 30 years.

Quick improvements that work:

-

Pay down credit card balances below 30% utilization (ideally below 10%)

-

Dispute any errors on your credit report through all three bureaus

-

Avoid opening new credit accounts in the 6 months before applying

-

Keep old credit cards open even if unused—credit history length matters

Step 2. Lower Loan-to-Value Below 75 Percent

Larger down payments directly reduce lender risk and unlock better rate tiers. The standard 20% down (80% LTV) gets you standard rates, but pushing to 25% down (75% LTV) or 30% down (70% LTV) can drop your rate by 0.25-0.5%.

On a $400,000 property, 20% down requires $80,000 while 25% down requires $100,000. That extra $20,000 might save you 0.375% on your rate, which equates to about $50 monthly or $18,000 over the loan term.

The trade-off? You're tying up more capital in one property instead of spreading it across multiple acquisitions. For portfolio builders, the 20% minimum often makes more sense than optimizing for the absolute lowest rate. For borrowers seeking maximum leverage, some DSCR lenders offer as little as 15% down.

Step 3. Document STR Income or Use Market Rent Analysis

Traditional lenders discount short-term rental income by 25-50% or ignore it entirely, forcing you to qualify on personal income alone. STR-specialized lenders through Rabbu's loan network recognize full Airbnb income potential using market data and comparable property performance.

Present your case with data: Use Rabbu's Market Data to show comparable properties in your target area generating $4,500-5,500 monthly. Export projections showing conservative estimates based on 65-70% occupancy rather than optimistic 85% projections.

For properties with existing STR history, provide 12-24 months of actual booking income from Airbnb or VRBO—this is the strongest possible documentation and often qualifies you for the best available rates.

Step 4. Reduce Personal Debt-to-Income Ratio

Even with DSCR loans that don't require personal income documentation, some lenders still consider your overall debt obligations. DTI below 43% is standard, but below 36% unlocks better pricing.

Strategic debt reduction approaches:

-

Pay off car loans or student loans with high monthly payments relative to remaining balance

-

Consolidate credit card debt to lower monthly minimums (though this might temporarily hurt credit score)

-

Wait to finance major purchases until after your investment property closes

-

Consider having rental income from existing properties counted toward income if you have 2+ years of tax returns showing it

Step 5. Shop Three or More Lenders in 14 Days

Multiple credit inquiries for the same loan type within 14-45 days (depending on credit scoring model) count as a single inquiry, protecting your credit score while you rate shop. This window lets you compare offers without penalty.

What to compare beyond just rate:

-

APR (annual percentage rate) includes fees and gives true cost comparison

-

Origination fees and closing costs: Some lenders advertise low rates but charge 2-3% origination

-

Prepayment penalties: Many DSCR loans include 1-3 year prepayment penalties

-

Rate lock periods: Ensure the lock covers your expected closing timeline

-

Lender reputation for actually closing on time

Rabbu's lender network pre-screens STR specialists and matches you with 2-4 lenders in 24-48 hours, streamlining the comparison process.

Where to Find Lenders That Understand Short-Term Rentals

Generic mortgage brokers and traditional banks rarely understand STR underwriting nuances. You want specialists who recognize that a $5,000/month Airbnb is fundamentally different from a $1,800/month long-term rental.

DSCR and Non-QM Specialists

DSCR lenders focus exclusively on investment property financing and understand cash flow underwriting. These aren't your neighborhood banks, they're specialized firms that originate loans specifically for real estate investors.

What sets them apart:

-

Underwriters trained in rental property analysis rather than W-2 employment verification

-

Loan products designed for portfolio scaling without arbitrary property limits

-

Technology platforms that speed processing and reduce documentation requirements

-

Willingness to consider STR income at full value rather than discounting it

Rabbu's lender network includes pre-vetted DSCR specialists who close deals in 21-30 days and understand vacation rental markets across the United States.

Local Banks Familiar With Vacation Markets

Community banks and credit unions in established vacation markets (Smoky Mountains, Florida Gulf Coast, Colorado ski towns) often have portfolio loan programs designed for local STR investors. They understand the seasonal income patterns and regulatory environment because they've financed dozens of similar properties.

The advantage? Relationship-based lending that considers your overall financial picture rather than checking standardized boxes. The disadvantage? Geographic limitations—they typically only lend in their immediate market area.

Rabbu-Vetted Lender Network (Recommended)

Rather than spending weeks calling lenders and explaining your strategy repeatedly, Rabbu's lender network matches you with 2-4 STR specialists in a matter of minutes. Each lender has been evaluated for actual experience closing STR deals, competitive DSCR and bank statement programs, transparent fee structures without hidden costs, proven track record of closing on time, and positive feedback from other STR investors.

The process takes minutes: Enter your target property location, purchase price, and basic financial information. Rabbu's system identifies lenders who operate in your market and offer appropriate programs for your profile, then connects you directly with loan officers who understand STR financing.

Why this matters for rates: STR-specialized lenders accurately assess your property's income potential and risk profile, often resulting in better effective rates than conventional lenders who don't understand the business model and compensate with overly conservative underwriting.

Find a Lender that Specializes in Short-Term Rentals

Connect with lenders who actually understand short-term rental cash flow and offer DSCR loans, portfolio financing, and investor-friendly terms.

Get Matched with STR LendersSecure Low Rates and Higher Short-Term Rental Returns With Rabbu

The best investment property loan rate is meaningless without a property that generates strong cash flow and appreciation potential. Rabbu integrates property discovery, financial analysis, and specialized lending in one platform—eliminating the fragmentation that slows most investors.

Your complete STR investment workflow:

-

Identify top-performing markets using Market Finder to target areas with strong occupancy rates, growing ADRs, and favorable regulations

-

Analyze specific properties with the Airbnb Calculator to generate professional-grade projections that strengthen your loan application

-

Browse turnkey listings on Rabbu's marketplace featuring properties with verified income history that qualify for better rates

-

Get matched with STR-specialized lenders through Rabbu's financing network who understand vacation rental underwriting

-

Connect with experienced agents using Rabbu's Agent Finder who negotiate based on cash flow rather than just comparable sales

The integrated advantage: When you present a lender with a property from Rabbu's marketplace (showing actual income history), projections from Rabbu's Calculator (based on verified market data), and analysis from Rabbu's Market Finder (demonstrating strong fundamentals), you're not just another loan application—you're a sophisticated investor with data-backed underwriting that justifies competitive rates.

The difference between struggling to close one deal per year through traditional channels and building a portfolio of 5-10 properties comes down to using specialized tools and lender relationships designed specifically for STR investing.

Frequently Asked Questions About Investment Property Loan Rates

Can I use projected Airbnb income before the property is operating?

Most DSCR lenders accept projected STR income based on comparable properties in the area, though rates might be 0.125-0.25% higher than for properties with verified operating history. Use Rabbu's Calculator to generate credible projections based on actual market data—lenders trust third-party validated numbers over applicant estimates. Properties with 12+ months of actual Airbnb income history qualify more easily and often receive better rates because lenders see proven performance rather than projections.

How many financed properties can I hold before rates increase again?

Conventional loans typically cap investors at 10 financed properties before requiring portfolio lending with higher rates. DSCR loans through Rabbu's lender network have no arbitrary limits—each property is underwritten individually based on its cash flow, so investors with 15, 20, or 30+ properties face the same qualification criteria as those buying their second property. Your rate is determined by credit score, down payment, and DSCR ratio rather than portfolio size.

Are interest-only investment loans too risky for short-term rentals?

Interest-only loans maximize cash flow by eliminating principal payments for 5-10 years, though you're not building equity through amortization. They work well for experienced investors in high-appreciation markets where equity growth comes from market appreciation rather than loan paydown, or for those planning to sell within the interest-only period. The risk comes at the end of the term when payments jump significantly or you face refinancing—if rates have increased or the property hasn't appreciated as expected, you might face challenges. Most conservative investors prefer traditional amortizing loans for long-term holds.

How do DSCR loans compare to conventional investment property loans?

DSCR loans qualify you based on property income rather than personal W-2 income, typically allowing 15-20% down payments and closing in 21-30 days. Rates run 0.5-1% higher than conventional loans (7.0-8.25% vs. 6.5-7.25%), but you avoid the 10-property limit, extensive income documentation, and personal DTI requirements. For self-employed investors or those building portfolios, the slightly higher rate is offset by the ability to close multiple deals per year without hitting qualification barriers. Conventional loans work best for W-2 employees with strong documented income buying their first 1-2 properties.

Don't Let Financing Kill Your Deal

Most banks don't understand short-term rentals. These lenders do.

Find a Lender