In this guide, we’ll walk you through the financing options available, including traditional mortgages, portfolio loans, and DSCR (Debt Service Coverage Ratio) loans. You’ll also learn how Rabbu’s expertise can help streamline this process, from analyzing the property’s potential to securing suitable financing solutions.

Table of Contents

- Why Invest in an Airbnb Property?

- Financing Challenges for Short-Term Rentals

- Traditional Mortgages for Airbnb Properties

- Portfolio Loans: A Flexible Option

- DSCR Loans: Tailored for Real Estate Investors

- Key Steps to Secure Financing

- How Rabbu Supports Airbnb Property Investors

- Frequently Asked Questions

- Conclusion

1. Why Invest in an Airbnb Property?

- High Cash Flow Potential: Short-term rentals often command higher nightly rates compared to long-term rentals.

- Flexible Usage: You can rent your property seasonally or year-round, depending on market demand.

- Asset Appreciation: Real estate generally appreciates over time, adding value to your investment beyond monthly cash flow.

Pro Tip: Use tools like Rabbu’s property analysis to evaluate a potential Airbnb’s earning potential, occupancy rates, and operating costs.

2. Financing Challenges for Short-Term Rentals

- Income Verification: Traditional lenders often prefer stable, documented income streams. Airbnb income can be variable, making it harder to qualify.

- Property Location: Some lenders have stricter guidelines for properties in vacation or tourist areas.

- Higher Down Payments: Financing an investment property typically requires a higher down payment (often 20% or more).

Insight: Understanding these challenges before shopping for loans can help you pick the right financing type for your investment goals.

3. Traditional Mortgages for Airbnb Properties

- Conventional Loans: Best for investors with strong credit and W-2 income.

- Pros: Often come with lower interest rates and standardized underwriting.

- Cons: Might require proof of stable income; short-term rental income is not always recognized fully by lenders.

Usage Tip: Traditional mortgages are ideal if you plan to keep the property for the long term and can document sufficient income outside of Airbnb revenue.

4. Portfolio Loans: A Flexible Option

- Definition: Portfolio loans are offered by lenders who keep the mortgage in their own investment portfolio instead of selling it on the secondary market.

- Pros: Flexible underwriting guidelines, can consider higher risk profiles or special property types.

- Cons: Rates might be slightly higher due to increased lender risk.

Who Benefits? Investors with multiple properties, or those with fluctuating income from short-term rentals, may find portfolio loans more accommodating.

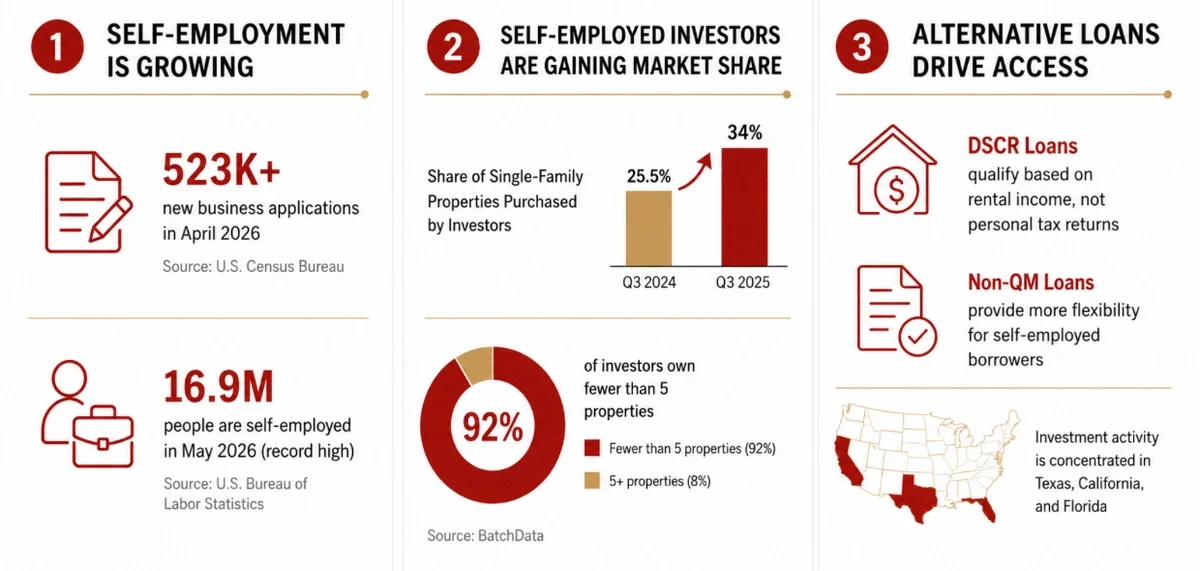

5. DSCR Loans: Tailored for Real Estate Investors

- What is DSCR? DSCR (Debt Service Coverage Ratio) measures a property’s income relative to its debt obligations. DSCR = Net Operating Income (NOI) / Total Debt Service (TDS)

- Pros: Approval primarily hinges on the property’s cash flow, not on borrower’s personal income.

- Cons: Usually require higher credit scores and down payments, but can be a perfect fit for investors with solid rental income projections.

Ideal Scenario: If your Airbnb has a track record of consistent rental revenue or you can project stable occupancy, a DSCR loan can be more accessible than a traditional loan.

6. Key Steps to Secure Financing

1. Evaluate Your Financial Health

Check your credit score, debt-to-income ratio, and liquid assets.

2. Define Your Investment Goals

Are you focused on cash flow, long-term appreciation, or portfolio expansion?

3. Research Potential Lenders

Compare rates, terms, and underwriting guidelines.

4. Prepare Thorough Documentation

Include projected rental income from Airbnb and a well-researched business plan.

5. Work With Real Estate Professionals

Real estate agents, property management companies like Rabbu, and mortgage brokers can guide you through local regulations and market conditions.

7. How Rabbu Supports Airbnb Property Investors

- Property Analysis: Rabbu’s platform can provide comprehensive insights into projected rental income and ROI, helping you and potential lenders see the property’s value.

- Financing Connections: Rabbu has industry relationships that can connect you with specialized lenders who understand short-term rental investing.

- Management Services: Once you secure financing, Rabbu helps manage your Airbnb to maximize occupancy and returns.

Value Add: By leveraging Rabbu’s expertise, you streamline the entire process—from discovering lucrative markets to sourcing the right loans and managing the property successfully.

8. Frequently Asked Questions

1. Can I use Airbnb income to qualify for a loan?

Many lenders are now considering Airbnb or short-term rental income, especially if you can show a history of stable bookings.

2. Is a higher down payment always required for short-term rental properties?

Most investment properties do require higher down payments, but some specialized lenders or loan programs may offer more flexible terms.

3. What documents are needed to get a DSCR loan?

You’ll typically need rent rolls or Airbnb income projections, plus standard documents like credit reports and property details.

9. Conclusion

How to finance an Airbnb property doesn’t have to be a daunting question. By understanding your financing options—whether it’s a traditional mortgage, a flexible portfolio loan, or a DSCR loan—you’ll be better equipped to make an informed decision. With Rabbu’s specialized knowledge in the short-term rental market, you can confidently invest in Airbnb properties that promise strong returns and long-term growth.