Traditional banks reject short-term rental loans because their underwriting systems weren't designed for vacation rental income—they discount your $5,500 monthly Airbnb revenue to $1,800 based on long-term rental comparables, or ignore it completely. Alternative lenders flip this equation: they qualify you based on your property's cash flow potential rather than your W-2 earnings, enabling you to acquire profitable STR properties that conventional financing would never approve.

This guide shows you how alternative lending works for STR investors, which loan products accelerate portfolio growth, and how to strengthen your application using market data and income projections that specialized lenders actually recognize.

What Is Alternative Lending For Short-Term Rentals

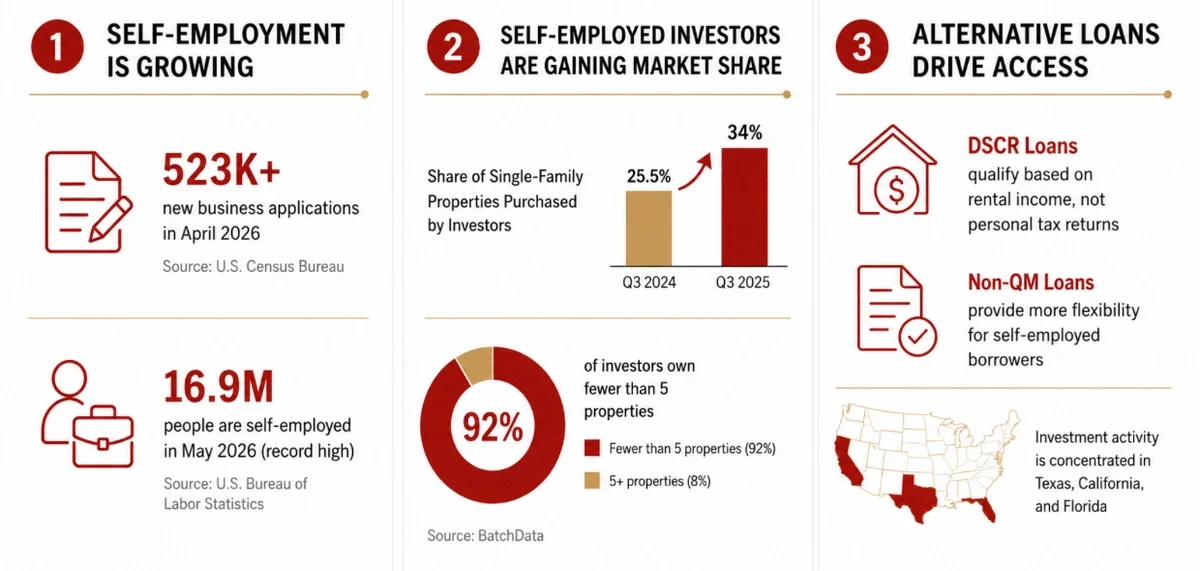

When traditional banks deny your loan application, alternative lending offers financing options specifically designed for short-term rental investors who don't fit conventional underwriting requirements. These specialized lenders qualify you based on your property's projected Airbnb income rather than your personal W-2 earnings or tax returns.

The fundamental difference comes down to how lenders evaluate risk. Alternative lenders understand that a property generating $5,500 monthly from Airbnb bookings represents stronger collateral than traditional underwriters acknowledge. Conventional banks might discount that same income to $1,800 based on long-term rental comparables—or ignore it entirely—while specialized STR lenders recognize the full cash flow potential.

Why Conventional Banks Often Reject Short-Term Rental Loans

Traditional lenders view STR income as unpredictable compared to long-term lease agreements, even though well-located vacation rentals consistently outperform traditional rentals. This perception gap creates systematic rejection for investors pursuing profitable rental strategies.

Banks reject STR loans for several reasons:

-

Rental income uncertainty: Banks discount STR revenue projections despite historical market data, treating $6,000 monthly Airbnb income the same as speculative business projections

-

Regulatory concerns: Zoning restrictions and permit requirements trigger automatic denials, even in markets with established STR frameworks

-

Limited STR expertise: Traditional underwriters lack vacation rental market knowledge, applying long-term rental formulas to properties designed for nightly bookings

-

Personal income requirements: Banks ignore property income potential entirely, forcing you to qualify based solely on W-2 earnings

Self-employed investors face additional barriers. If you've legally minimized taxable income through business deductions, your tax returns might show $75,000 while your actual cash flow exceeds $200,000—but banks only see the lower number.

Don't Let Financing Kill Your Deal

Most banks don't understand short-term rentals. These lenders do.

Find a LenderAlternative Financing Options When Banks Say No

Alternative lenders offer multiple pathways to STR financing, each designed for different investor profiles and property types. Understanding the options helps you match the right loan structure to your specific situation.

1. DSCR Lenders (Recommended)

Debt Service Coverage Ratio loans qualify you based on property cash flow rather than personal income. These lenders calculate a simple ratio: monthly rental income divided by monthly debt obligations (mortgage, taxes, insurance, HOA fees).

If your property generates $4,800 monthly and total debt obligations equal $3,600, your DSCR is 1.33—well above the 1.0-1.25 minimum most lenders require. You qualify without submitting tax returns, W-2s, or employment verification letters. Rabbu connects you with vetted DSCR lenders who specialize in STR properties, typically offering 15-25% down payments and closing timelines of 15-30 days.

2. Asset-Based Hard Money Loans

Hard money lenders provide short-term financing (typically 6-24 months) secured primarily by property value rather than income or credit. Interest rates run higher—often 9-14%—but approval happens in days rather than weeks.

These loans work best for fix-and-flip scenarios or bridge financing when you close quickly on time-sensitive deals. You might use hard money to acquire a property requiring renovations, complete the work, establish STR income history, then refinance into a DSCR loan at lower rates.

3. Bridge Financing

Bridge loans provide temporary capital to acquire properties quickly before securing permanent financing. If you find a turnkey STR generating strong cash flow but face competing offers, bridge financing gives you speed advantage.

Rates typically fall between traditional mortgages and hard money—around 7-10%—with terms of 6-36 months. The strategy: close fast with bridge financing, operate the property for 6-12 months to establish income documentation, then refinance into a lower-rate DSCR loan.

4. Peer To Peer Lending Platforms

Online P2P platforms connect borrowers directly with individual investors willing to fund real estate deals. Platforms like LendingClub or Prosper aggregate capital from multiple lenders to fund your loan, often with more flexible underwriting than traditional banks. Interest rates vary widely based on your credit profile—typically 6-12% for investment properties, with funding occurring within 2-4 weeks.

5. Crowdfunding Portals

Real estate crowdfunding platforms like Fundrise or RealtyMogul allow you to raise capital from multiple investors for larger STR acquisitions or portfolio expansions. Investors contribute smaller amounts ($500-$50,000) in exchange for equity stakes or debt positions in your property. You maintain operational control while distributing returns based on agreed-upon terms.

6. Private Equity Or Joint Ventures

Partnership arrangements where investors provide capital in exchange for equity ownership offer another path when traditional financing isn't available. You might bring deal sourcing expertise and operational management while your partner contributes 100% of the capital for a 50/50 ownership split. Clear operating agreements defining responsibilities, profit distribution, and exit strategies are essential.

7. Seller Financing And Lease Options

Owner-financed deals eliminate lender involvement entirely—the seller acts as your bank, and you make payments directly to them over an agreed term. This approach works well when acquiring STR properties from retiring operators who want steady income without property management responsibilities. Lease-to-own arrangements provide another creative path: you lease the property with a portion of rent payments credited toward an eventual purchase.

8. Home Equity And Portfolio Loans

If you own a primary residence with substantial equity, a home equity line of credit (HELOC) or cash-out refinance can fund STR down payments. Rates typically run lower than investment property loans since your primary residence serves as collateral. Portfolio lenders who keep loans on their own books rather than selling to Fannie Mae or Freddie Mac offer customized solutions for investors with multiple properties.

Find a Lender that Specializes in Short-Term Rentals

Connect with lenders who actually understand short-term rental cash flow and offer DSCR loans, portfolio financing, and investor-friendly terms.

Get Matched with STR LendersHow To Choose The Right Loan For Your Airbnb Deal

Matching loan type to your specific investment strategy and property characteristics determines whether your deal generates strong returns or struggles with excessive debt service. Each financing option carries distinct tradeoffs in cost, speed, and qualification requirements.

Compare Interest Rates And Points

Look beyond headline interest rates to calculate true cost of capital including origination fees, points, and closing costs. A 7.5% loan with 2 points ($4,000 on a $200,000 loan) costs more over 12 months than an 8% loan with zero points. Use Rabbu's lending partner network to get quotes from multiple DSCR lenders simultaneously, comparing total cost rather than just rate.

Evaluate Speed To Close

Turnkey Airbnb properties with verified income history often receive multiple offers within 48 hours of listing. If you're competing against cash buyers or investors with established lending relationships, your ability to close in 15-21 days instead of 45-60 days can determine whether you win the deal. DSCR lenders typically close fastest—15-30 days—while conventional mortgages require 45-60 days minimum.

Check Prepayment Rules And Seasoning

Many alternative loans include prepayment penalties—typically 1-3 years—that charge fees if you refinance or sell early. A loan with a 3-year prepayment penalty might charge 3% of the loan balance if paid off in year one, 2% in year two, 1% in year three. Understand the terms before borrowing, especially if you plan to refinance into lower-rate conventional financing once you establish income history.

Align Term Length With Exit Strategy

Short-term loans (6-24 months) work well for fix-and-flip scenarios or bridge financing before permanent loans. Longer terms (15-30 years) suit buy-and-hold investors building rental portfolios for sustained cash flow. Match your loan term to your business plan—if you're converting a single-family home into an STR and plan to refinance after 12 months of operation, a 2-year bridge loan makes more sense than a 30-year mortgage.

Weigh Personal Versus Asset Guarantees

Some loans require personal guarantees making you liable for deficiency balances if foreclosure proceeds don't cover the debt. DSCR loans typically rely solely on property collateral, limiting your personal exposure. Non-recourse loans (no personal guarantee) allow you to scale with less personal risk, though they often carry slightly higher rates.

Steps To Strengthen Your Application With STR Income Data

Lenders approve applications backed by credible market data and realistic projections far more readily than applications based on optimistic guesswork. The following steps demonstrate you've done serious due diligence.

Step 1. Research Market Performance With Rabbu's Market Finder

Use Rabbu's Market Finder to identify top-performing STR markets based on actual occupancy rates, average daily rates, and investor returns. Focus on markets showing 65%+ occupancy, $150+ ADR, and 15%+ cash-on-cash returns for properties matching your target criteria. When you tell lenders "I'm targeting Gatlinburg because it shows 73% average occupancy and $220 ADR based on 450+ active listings," you demonstrate market knowledge that strengthens your application.

Step 2. Browse STR Listings With Historical Income or Accurate Projections

Search for Airbnbs for sale on Rabbu's marketplace of active STR listings. The marketplace has both turnkey Airbnbs for sale with historical operating income as well as prospective STR conversion opportunities with projected income based on real-time market data. Here’s how to apply filters on the marketplace to find the type of property you’re looking for:

-

Navigate to the Rabbu Marketplace

-

Select your chosen markets,

-

If you’re looking for a turnkey Airbnb, then click All Filters → Tags → Active Airbnb.

-

Active Airbnb = turnkey Airbnb listings with actual performance history.

-

Actual Financials = actual historical financials inputted by the seller or listing agent

-

-

Set price filters (typically >$300K) based on market norms.

-

Sort by Gross Yield, and filter results to 5–30% yield range.

-

Filter by property type, bedrooms, and amenities matching your target acquisition.

-

If you’re looking for a property with STR potential, add tags for Airbnb Potential, Former Airbnb and Agent Pick.

-

If too few results:

-

Include Public Listings (less vetted, but higher volume).

-

-

To stay updated, click Save Search → set up email alerts for new matching properties.

-

Note that you must have a Rabbu account to save a search (it’s free)

-

-

When you find a property you like, click Contact Agent to inquire

Important Note: Active Airbnb properties move fast — many transact within 48 hours. Contact agents immediately if something fits your criteria. Many of these are equivalent to “off market” properties—only listed on Rabbu’s marketplace and not found anywhere else.

The Best STR Deals Never Hit Zillow

Browse exclusive listings for turnkey Airbnbs with actual income data.

Search Exclusive ListingsStep 3. Build Realistic Cash Flow Projections With Rabbu's Calculator

Use Rabbu's Airbnb Calculator to create detailed proformas including seasonal variations, vacancy rates, cleaning costs, and management fees. Input your target property address to generate projections based on actual comparable performance rather than generic assumptions. Toggle between 75th and 90th percentile performance scenarios to show lenders both conservative and optimistic projections.

Step 4. Highlight Occupancy Regulations And Zoning Compliance

Demonstrate understanding of local STR laws, permit requirements, and HOA restrictions that might impact operations. Research whether your target property requires business licenses, occupancy taxes, or safety inspections, and document your compliance plan. Work with Rabbu's vetted agents who specialize in STR regulations and can verify zoning compliance before you make offers.

Step 5. Document Host Track Record Or Management Team

Present your experience managing STRs or identify established management companies from Rabbu's service provider network. If you're a first-time STR investor, partnering with a property manager showing 4.8+ ratings and 100+ managed properties reduces perceived risk. Include guest ratings and occupancy history from any properties you currently operate.

Step 6. Show Reserve Funds And Exit Plans

Demonstrate financial cushion beyond your down payment—typically 6-12 months of operating expenses including mortgage, utilities, insurance, and maintenance. Articulate your exit strategy if the property underperforms: will you convert to long-term rental or sell within 18 months? Clear contingency plans show sophisticated thinking.

Key Risks And Costs Of Non Bank Loans

Alternative lending opens doors traditional banks keep closed, but the opportunities come with tradeoffs you'll want to evaluate honestly. Understanding the downsides helps you make informed decisions about which financing path aligns with your risk tolerance.

Higher Rates And Fees

Alternative lenders typically charge 0.5-2% higher interest rates than conventional mortgages due to increased risk and faster processing. A conventional investment property loan might offer 6.5% while a DSCR loan from a specialized lender runs 7.5-8.5%. Budget for higher carrying costs but factor in increased purchasing power—if higher rates enable you to acquire a property generating 20% cash-on-cash returns that you couldn't buy with conventional financing, the rate differential becomes acceptable.

Shorter Terms And Balloons

Some alternative loans require refinancing or full payoff within short timeframes—often 3-10 years. Bridge loans might balloon after just 12-24 months, requiring you to either refinance into permanent financing or sell the property. DSCR loans typically offer longer terms (up to 30 years) compared to hard money or bridge options, though some include balloon provisions after 5-7 years.

Variable Or Adjustable Payments

Some loans carry floating rates tied to prime rate or SOFR indexes, meaning your payment can increase if benchmark rates rise. A loan starting at 7.5% might adjust to 9% if the underlying index increases 1.5 points. Understand payment fluctuation risks and model worst-case scenarios using Rabbu's free Airbb Calculator—if a 2% rate increase would eliminate your positive cash flow, that loan carries more risk.

Appraisal And Legal Expenses

Alternative loans may require specialized STR appraisals analyzing income potential rather than just comparable sales. The appraisals cost $500-$1,000 more than standard residential appraisals and take longer to complete. Factor in closing costs of 2-5% of loan amount including origination fees, title insurance, attorney fees, and appraisal costs.

Impact On Cash Flow

Higher payments reduce property profitability, potentially turning a strong deal marginal. A property generating $4,800 monthly might show excellent returns with a $2,800 conventional mortgage payment but barely break even with a $3,900 alternative loan payment. Use Rabbu's Investor Return Calculator to verify deals still generate positive cash flow after financing costs.

Next Moves To Fund Your First Or Next Airbnb Faster

The old way of STR investing required juggling multiple tools, hunting for market data across various platforms, and working with professionals who didn't understand the vacation rental business model. The new way is simpler: use Rabbu's integrated platform to identify profitable markets, analyze active STR listings with verified income data, and connect with specialized lenders.

Your next steps:

-

Identify Your Market: Use Rabbu's Market Finder to discover top-performing STR markets based on occupancy rates, average daily rates, and investor returns

-

Browse Profitable Properties: Explore Rabbu's marketplace of active STR listings showing verified income history and STR-potential properties with data-backed projections

-

Get Pre-Qualified: Connect with Rabbu's DSCR lending partners for fast, property-based financing that ignores personal income requirements

The Rabbu platform was specifically designed to make this process easy for investors like you. Whether you’re a seasoned investor or looking to make your first STR investment, there’s no reason for financing to kill your deal. We’ve helped thousands of Airbnb investors get financing who were previously turned down by traditional banks like Wells Fargo and Bank of America.

Find a Lender that Specializes in Short-Term Rentals

Connect with lenders who actually understand short-term rental cash flow and offer DSCR loans, portfolio financing, and investor-friendly terms.

Get Matched with STR LendersFAQs About Alternative Lending For Short Term Rentals

Can alternative lenders finance short term rental properties in any location?

Yes, as long as the underlying financials make sense from an underwriting perspective. We suggest reaching out to the lenders in our network who specialize in financing Airbnb investment properties to get pre-approval.

How much down payment do alternative STR lenders typically require?

Alternative lenders usually require larger down payments than traditional mortgages to offset increased risk. DSCR lenders typically require 15-25% down, while hard money lenders may require 25-40% depending on loan type, property condition, and your credit profile.

What happens if my short term rental income drops after getting alternative financing?

Most alternative loans focus on property value rather than ongoing income verification, but cash flow problems can still trigger default if you cannot make monthly payments. Maintain adequate reserves (6-12 months operating expenses) for market downturns and use Rabbu's market data to understand seasonality patterns.

How quickly can I close with alternative STR financing?

DSCR lenders typically close in 15-30 days once you submit complete documentation, while hard money lenders may close in 7-14 days for time-sensitive deals. Speed depends on property type, appraisal complexity, title issues, and how quickly you provide requested documentation.

Do I need STR experience to qualify for alternative financing?

Many DSCR lenders focus on property performance projections rather than operator experience, though demonstrating STR knowledge strengthens your application. Use Rabbu's platform to provide market research, realistic projections, and professional partnerships that compensate for limited personal experience.

Don't Let Financing Kill Your Deal

Most banks don't understand short-term rentals. These lenders do.

Find a Lender