Short-term rentals can generate more cash flow than traditional rentals, sometimes by 2–3x. But most investors never get past their first or second property.

Most investors don’t fail because of bad properties.

They fail because their financing can’t keep up.

Banks don’t count Airbnb income.

That’s the bottleneck.

Not the deal—the approval process.

They want tax returns, W-2s, and stable salaries—things most investors either don’t have or intentionally minimize.

So even when your property performs, you hit a wall.

This guide breaks down exactly how to:

- Start a short-term rental business

- Analyze profitable Airbnb deals

- Finance properties using DSCR loans

- Scale into a real portfolio

What Is a Short-Term Rental Property?

A short-term rental (STR) is a property rented out on a nightly or weekly basis through platforms like Airbnb or VRBO.

Instead of fixed rent, you:

- Charge per night

- Adjust pricing based on demand

- Optimize occupancy and revenue

This creates higher income potential—but requires a more strategic approach.

Why Short-Term Rentals Are Profitable in 2026

Investors are shifting toward short-term rentals for one reason: Cash flow.

Short-Term Rental Market Snapshot (2026)

- 1.1M+ U.S. listings

- ~$358 average daily rate

- ~39% occupancy rate

- Growing faster than hotel demand

The U.S. short-term rental market includes over 1.1 million active listings, with average daily rates around $358 and strong occupancy levels driving investor demand.

Airbnb operates in over 220 countries with more than 5 million hosts and over 2 billion guest arrivals, highlighting the scale of the short-term rental economy.

Traditional rentals are predictable but capped.

Short-term rentals are dynamic and often more profitable.

The opportunity is real.

The challenge is qualifying and moving fast enough to take advantage of it.

Key Benefits of Short-Term Rentals

Short-term rentals can generate significantly more income than traditional rentals—when done right. For investors focused on cash flow and scaling, they offer clear advantages that traditional properties can’t match.

- Higher Income Potential: Top STR markets consistently outperform long-term rentals.

- Dynamic Pricing Power: Rates increase during weekends, holidays, and peak seasons.

- Tax Advantages: Short-term rentals can unlock depreciation and advanced tax strategies.

- Scalable Investment Model: With the right financing, you’re not limited by personal income.

How to Start a Short-Term Rental Business Step-by-Step

Success in short-term rentals comes down to execution. Investors who win focus on the fundamentals early: the market, the numbers, and demand.

This isn’t about buying a vacation home.

It’s about building an income-producing asset that performs.

Step 1: Choose the Right Market

Your market determines your income before you ever buy the property.

The biggest mistake new investors make is choosing a location based on personal preference instead of performance. A great property in the wrong market will underperform. An average property in the right market can outperform expectations

Focus on areas with:

- Strong tourism demand

- Business travel activity

- Seasonal or event-driven traffic

Top-performing short-term rental markets typically include:

- Beach destinations

- Mountain towns

- Urban cores

The market does most of the work.

Get this wrong, and nothing else matters.

Bottom line: Don’t guess. Use real data to confirm that the market supports consistent bookings and strong revenue.

Step 2: Analyze an Airbnb Investment Property

You’re not buying a home. You’re buying an income-producing asset. Tools like Rabbu track performance across more than 10 million short-term rental listings, giving investors real data on occupancy, pricing, and revenue potential.

Access to real-time Airbnb data, such as pricing, occupancy, and reviews, allows investors to evaluate deals with far greater accuracy than traditional rental analysis

Focus on:

- Average daily rate (ADR)

- Occupancy rate

- Monthly revenue projections

Bottom line: Use tools like AirDNA and comparable listings to estimate income.

Step 3: Design for Bookings

Design isn’t about aesthetics—it’s about revenue.

The way your property looks, functions, and photographs directly impacts:

- Booking rate

- Nightly price

- Overall occupancy

Most guests are comparing dozens of listings at once. If your property doesn’t stand out, it doesn’t get booked.

Prioritize:

- Guest capacity: More beds = higher revenue potential

- Unique features: Hot tubs, views, game rooms, themed spaces

- Professional photography: Your listing is only as strong as your photos

Top-performing short-term rentals are designed with one goal: to maximize clicks, bookings, and nightly rates

You should also consider:

- Layout and flow for larger groups

- Amenities that justify higher pricing

- Visual appeal in listing thumbnails

Bottom line: Design it to compete, not just to look good.

Step 4: Understand Local STR Regulations

Nearly 80% of major short-term rental markets now have regulations in place, making compliance a critical part of any STR investment strategy.

Before you buy:

- Confirm zoning laws

- Verify STR permits

- Check occupancy limits

Bottom line: Ignoring this step can eliminate your ability to operate.

Step 5: Automate or Hire Management

Short-term rentals aren’t passive—they’re operational businesses.

Without the right systems in place, managing bookings, guests, and turnover can quickly become overwhelming. The difference between average and high-performing properties often comes down to how efficiently they’re managed.

You have two options:

- Self-manage for higher margins and full control

- Hire a short-term rental property manager for a more hands-off approach

Most investors start by self-managing, then transition to systems or management as they scale. Regardless of your approach, automation is critical.

Focus on automating:

- Guest communication, like inquiries, check-in instructions, reviews

- Cleaning and turnover coordination

- Dynamic pricing adjustments based on demand

Tools and platforms can streamline these processes, reduce manual work, and improve consistency across bookings.

Bottom line: Treat your short-term rental like a business. The more you systemize and automate, the easier it is to scale.

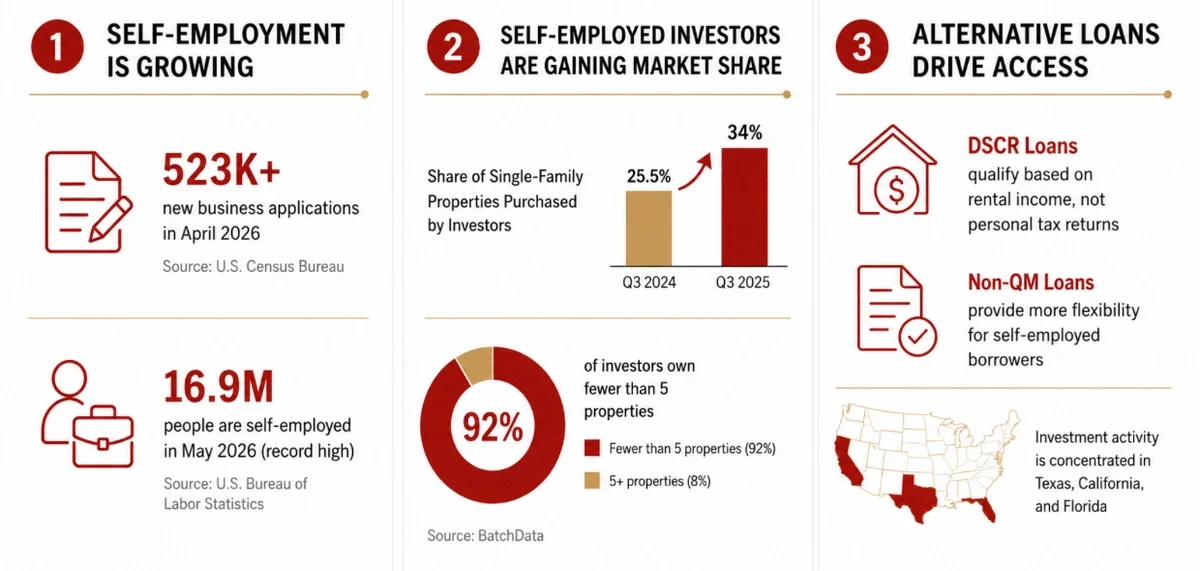

How to Finance a Short-Term Rental Property

This is where most investors get stuck.

Traditional lenders:

- Don’t count Airbnb income

- Require W-2s or tax returns

- Limit how many properties you can finance

That model wasn’t built for investors, and it breaks down fast when you try to scale.

The reality is that if your financing strategy depends on your personal income, your portfolio will always be limited.

The Solution: Financing Based on Property Income

Instead of qualifying based on your job, there’s a better approach: qualify based on the property’s cash flow.

This is how experienced investors finance short-term rentals and scale beyond one or two properties.

Lenders evaluate:

- Projected rental income (often using AirDNA or market comps)

- Monthly debt obligations

- Overall deal strength

Not your tax returns.

Successful investors keep buying—while everyone else stalls out.

Why This Matters for Short-Term Rental Investors

Short-term rental income doesn’t fit traditional underwriting since it’s:

- Variable

- Seasonal

- Often underreported on tax returns

That’s why investors need financing designed specifically for income-producing properties, not personal income profiles.

You shouldn’t be penalized for how you make money.

Your property should speak for itself.

Bottom line: The right financing strategy doesn’t just help you buy one property—it determines how fast you can grow.

DSCR Loans for Short-Term Rentals Explained

A DSCR loan (Debt Service Coverage Ratio loan) allows you to qualify based on the property’s income, not your personal income.

- No tax returns.

- No W-2s.

- No income limitations.

DSCR loans flip the traditional approval process. Instead of asking what you earn, lenders ask one question: Does the property generate enough income to cover the loan?

If the deal cash flows, you can qualify, regardless of your personal income. This is what makes DSCR loans ideal for Airbnb and short-term rental investors, where income is driven by the property rather than a W-2.

DSCR Formula Explained

DSCR = Rental Income / Debt Payments

- 1.0 = Break-even (income covers the mortgage)

- 1.25+ = Strong investment (preferred by most lenders)

The higher the DSCR, the lower the risk, and the easier the approval.

Bottom line: If your short-term rental produces consistent income, you can qualify—and scale—without being limited by your personal finances.

Start your DSCR approval with MMC Lending.

DSCR Loan Requirements for Short-Term Rental Properties

DSCR loans are flexible—but the deal still has to make sense.

Typical DSCR Financing Requirements

- Credit score: 620–700+

- Down payment: 20–25%

- DSCR ratio: 1.0–1.25+

- Property income projections

How Non-Traditional Lenders Evaluate Short-Term Rental Deals

Understanding underwriting gives you an edge.

- DSCR Ratio: This is the primary approval factor. If your deal barely breaks even, it’s risky. Stronger cash flow = stronger approval.

- Income Validation: Lenders rely on rental comps, historical data (if available), and market projections. Projected income may be discounted to account for vacancy.

- Loan-to-Value (LTV): Expect a 70–80% LTV and 20–30% down payment. Higher leverage = stricter requirements.

- Credit Profile: The typical minimum is 620. Stronger borrowers get better terms.

DSCR vs Traditional Loans: Which Is Better for Short-Term Rentals?

Choosing the right financing structure isn’t just important; it determines how far you can scale.

Most investors start with traditional mortgages. That works—until it doesn’t. Short-term rentals don’t fit the way banks underwrite loans.

From a lender’s perspective, that makes STR income look inconsistent, even when the property performs.

That’s where traditional financing breaks down.

Traditional Mortgage

Traditional loans are built for salaried borrowers—not investors.

Pros:

- Lower interest rates

- Long-term stability

Cons:

- Requires W-2 income or tax returns

- Airbnb income is often ignored or undervalued

- Debt-to-income (DTI) limits cap how many properties you can own

Translation: Even if your properties' cash flow is good, your personal income becomes the bottleneck.

DSCR Loan

DSCR loans are built for investors. Instead of focusing on you, they focus on the deal.

Pros:

- Qualify based on property income—not personal income

- No tax returns or W-2s required

- No DTI limits restricting portfolio growth

Cons:

- Slightly higher interest rates

- Requires a strong, cash-flowing deal

Translation: If the property works, you can keep buying.

The Bottom Line

- Buying 1–2 properties → traditional financing may work

- Scaling a portfolio → traditional financing will slow you down

DSCR loans remove the biggest constraint in real estate investing: your personal income

Common Short-Term Rental Investing Mistakes

Avoid these if you want consistent returns.

- Overestimating Revenue: Always use conservative projections.

- Ignoring Seasonality: Demand fluctuates throughout the year.

- Not Checking Regulations: Some markets completely restrict STRs.

- Buying Based on Emotion: This is a business—not a vacation home.

- Using the Wrong Financing: Traditional loans slow growth.

How to Scale a Short-Term Rental Portfolio

This is where the real opportunity is. Short-term rentals continue gaining market share from hotels, reinforcing long-term demand and investment potential.

Step 1: Buy for Cash Flow

Cash flow fuels growth—not appreciation.

Step 2: Stabilize the Property

- Improve occupancy

- Increase pricing efficiency

- Optimize guest experience

Step 3: Leverage the Asset

Use DSCR loans to:

- Refinance

- Access equity

- Fund new purchases

Step 4: Repeat

This is how investors go from:

- 1 property → 5

- 5 properties → 20+

DSCR financing removes the income ceiling that stops most investors.

Ready to finance your next property?

Is Short-Term Rental Investing Right for You?

Short-term rentals are ideal if you:

- Want higher cash flow potential

- Are self-employed or write off income

- Plan to scale your portfolio

They may not be ideal if you:

- Want passive, hands-off investing

- Prefer fixed monthly income

Final Thoughts on Short-Term Rental Investing

Short-term rentals offer one of the best opportunities in real estate today—but only if you approach them strategically.

It comes down to two things:

- Buying the right deal.

- Using the right financing.

Traditional lenders weren’t built for this.

DSCR loans were.

- No tax returns.

- No W-2s.

- No unnecessary barriers.

Qualify based on what actually matters—your property’s income.

Start your short-term rental financing strategy today.

Don't Let Financing Kill Your Deal

Most banks don't understand short-term rentals. These lenders do.

Short-Term Rental Investing FAQs

What is a short-term rental property?

A short-term rental (STR) is a property rented out for short stays—typically nightly or weekly—through platforms like Airbnb or VRBO. Unlike traditional rentals, STRs generate income based on occupancy and nightly rates rather than fixed monthly rent.

Are short-term rentals more profitable than long-term rentals?

Yes—short-term rentals can be more profitable, especially in high-demand markets. They allow investors to charge higher nightly rates and adjust pricing based on seasonality, events, and demand. However, profitability depends on occupancy rates, expenses, and local regulations.

How do you finance a short-term rental property?

Short-term rental properties can be financed using:

- Traditional mortgages (limited flexibility)

- DSCR loans (most common for investors)

DSCR loans are typically the best option because they allow you to qualify based on the property’s rental income rather than personal income.

What is a DSCR loan for short-term rentals?

A DSCR loan (Debt Service Coverage Ratio loan) is a type of investment property loan that qualifies borrowers based on the property’s income.

Instead of requiring tax returns or W-2s, lenders evaluate whether the rental income can cover the mortgage payments.

What DSCR is required for an Airbnb loan?

Most lenders require:

- Minimum DSCR: 1.0 (break-even)

- Preferred DSCR: 1.25 or higher

A higher DSCR increases your chances of approval and better loan terms.