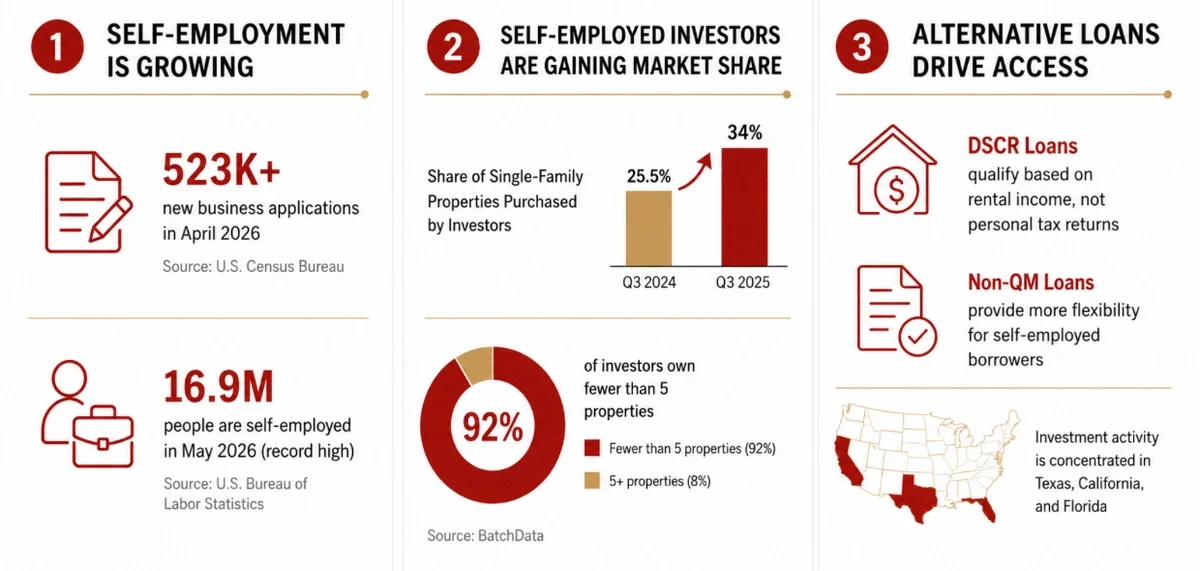

Real estate investors are always on the lookout for financing options that work with their investment strategy. One loan product that has been making waves in the industry is the DSCR loan (Debt Service Coverage Ratio loan). This type of financing prioritizes the income-generating potential of a property over the borrower’s personal finances.

If you're an investor, understanding how a DSCR loan works could be a game-changer for your portfolio. Let’s dive into what DSCR loans are, how they’re calculated, and why we recommend them for growing your real estate investments.

Key Takeaways:

-

DSCR loans are ideal for rental investors and those with unconventional income sources.

-

Loan approval is based on property income, not personal financials.

-

The DSCR equals net operating income divided by debt service, including principal and interest.

-

Short-term rental investors can benefit from higher cash flow potential.

What Is a DSCR Loan?

A Debt Service Coverage Ratio (DSCR) loan is a financing option designed for real estate investors. Unlike conventional mortgages that assess personal income and creditworthiness, DSCR loans focus on a property’s ability to generate sufficient rental income to cover its debt obligations.

Main Benefits of DSCR Loans:

-

No Personal Income Verification – Loan approval is based on property cash flow, not borrower income.

-

Ideal for Rental Investors – Perfect for short-term and long-term rental properties.

-

Faster Approval Process – Streamlined documentation compared to traditional mortgages.

-

Scalable Financing – Enables investors to acquire multiple properties based on rental income.

How Is DSCR Calculated?

Lenders determine loan eligibility by calculating the Debt Service Coverage Ratio (DSCR):

DSCR Formula:

DSCR = Net Operating Income (NOI) ÷ Total Debt Service

-

Net Operating Income (NOI): Total rental income after deducting operating expenses (e.g., taxes, insurance, property management fees).

-

Total Debt Service: The annual loan payments, including principal and interest.

Example Calculation:

If a rental property generates an NOI of $120,000 and annual debt payments total $100,000:

DSCR = $120,000 ÷ $100,000 = 1.2

-

A DSCR of 1.2 means the property generates 20% more income than required to cover its debt payments.

-

Most lenders require a DSCR of 1.2 to 1.5 depending on market conditions.

Why Choose a DSCR Loan?

1. Property Cash Flow Over Personal Income

-

Suitable for self-employed investors or those with non-traditional income streams.

-

Approval is based on rental income potential rather than tax returns or W-2s.

2. Scalable Real Estate Investing

-

Investors can acquire multiple properties as long as each meets DSCR requirements.

-

Helps grow portfolios faster without personal debt constraints.

3. Streamlined Loan Approval Process

-

Less paperwork compared to traditional bank loans.

-

Faster closings with reduced income verification requirements.

4. Recommended for Short-Term Rentals

DSCR loans are ideal for short-term rental properties that generate higher yields than traditional rentals.

Challenges of DSCR Loans

While DSCR loans offer flexibility, they also come with potential downsides:

1. Higher Interest Rates

-

Lenders perceive DSCR loans as riskier and may charge slightly higher rates compared to conventional mortgages.

2. Larger Down Payments

-

Typically requires 20-25% down to secure financing.

-

Ensures lenders mitigate risk but requires more capital upfront.

3. Market Sensitivity

-

Rental income fluctuations due to vacancies, market downturns, or regulatory changes can impact DSCR compliance.

Expert Tip:

We advise investors to analyze potential cash flow fluctuations and factor in worst-case scenarios before committing to a DSCR loan.

Who Should Use a DSCR Loan?

A DSCR loan is an excellent option for investors who:

-

Own or plan to purchase rental properties.

-

Want to expand their portfolio without personal income restrictions.

-

Have non-traditional income sources (self-employed, freelancers, or real estate professionals).

Why DSCR Loans Work for Short-Term Rentals

-

Higher rental income potential increases DSCR eligibility.

-

Short-term rentals often generate better cash flow than long-term leases.

Final Thoughts

A DSCR loan is a powerful financing tool for real estate investors looking to scale without personal income limitations. By prioritizing property cash flow over personal financials, these loans offer a flexible, scalable, and efficient way to grow your investment portfolio. Work with trusted partners like Rabbu to ensure your investment is set up for success.