On July 11, 2026, the 21st Century ROAD to Housing Act became law. It cleared the Senate 85-5 on June 22 and the House 358-32 on June 23, and it took effect without a presidential signature after the required window passed. It is the largest federal housing package in decades.

Most of the coverage has focused on one section, the one that restricts large investors from buying single-family homes. The headlines have been broad enough that a lot of short-term rental buyers are now asking a reasonable question: does this stop me from buying an Airbnb?

No. Here is the detail behind that answer, and the parts of the law that actually matter to you.

The dates that matter

The restriction is not in force yet. Nothing about the law requires anyone to sell anything.

| Milestone | Date |

|---|---|

| Became law | July 11, 2026 |

| Purchase restriction takes effect | 180 days after enactment (approximately January 7, 2027) |

| First HUD status filing due from covered investors | Within 180 days of enactment, then annually by December 31 |

| Transitional purchases from non-covered sellers allowed until | Two years after the effective date |

| Provision sunsets | 15 years after the effective date |

Two important things are worth noting. The restriction is not retroactive, so existing portfolios are untouched. An earlier draft that would have forced covered investors to divest over seven years was dropped from the final bill. That single change is why the reaction across the single-family rental and build-to-rent sectors has been closer to relief than alarm.

Who the law actually applies to

Section 1001 is titled "Homes Are for People, Not Corporations." It bars a "large institutional investor" from purchasing additional single-family homes unless the purchase fits an exception.

The definition has two prongs, and an entity has to meet both.

| Prong | Test |

|---|---|

| Business | A for-profit entity or business arrangement engaged, in whole or in part, in investing in, owning, renting, managing, or holding single-family homes |

| Scale | Alone or in concert with other entities, directly or indirectly, has investment control of 350 or more single-family homes in the aggregate |

Two supporting definitions do a lot of work here.

Single-family home means a structure with two or fewer dwelling units intended for residential occupancy. Manufactured homes are excluded. Individually platted townhomes may well be included.

Investment control is broader than ownership. It covers owning the home, holding primary authority or fiduciary responsibility over material investment or management decisions, controlling the general partner or managing member, controlling the investment manager or advisor, or owning more than 25% of any class of equity in the owning entity unless you are a passive investor.

Penalties run to $1 million per violation or three times the purchase price, whichever is greater.

Why this is not a STR law

The phrase "short-term rental" does not appear in the Act. Neither does "vacation rental." STR regulation remains what it has always been: a local question decided city by city and county by county. Nothing in this law changes a permit cap, an occupancy rule, or a registration requirement anywhere.

The threshold is the other half of the answer. The typical STR buyer owns one to five properties. A large regional operator might own twenty or thirty. Getting to 350 homes under common investment control is a different category of business entirely, and it is not one the short-term rental market is built out of. STR ownership in the United States remains overwhelmingly individual investors and small operators.

There is also a structural reason institutional capital has stayed out. Short-term rentals require hospitality operations: guest management, dynamic pricing, turnover, reviews. Institutional single-family capital has consistently preferred long-term rentals and build-to-rent precisely because those assets do not require any of that. The law lands squarely on the segment that was already not competing with you.

The exceptions

The list of excepted purchases is long enough that the practical effect on institutional strategy is redirection rather than prohibition.

- Build-to-rent. Newly constructed single-family homes managed as rentals are exempt, whether in an all-rental community or a mixed owner-and-renter community.

- For-sale product. Newly constructed, renovated, or converted homes intended for sale are exempt.

- Renovate-to-rent. Substantial rehabilitation of homes failing structural or core system code elements, with improvements of at least 15% of purchase price.

- Homeownership programs. Rent-to-own style structures with rental payment reporting to credit bureaus and meaningful financial support toward the renter's purchase.

- Senior housing. Newly built, renovated, or converted product operated for households with a member aged 55 or older.

- Debt and servicing. Repossession, foreclosure, deed-in-lieu, and loss mitigation acquisitions, provided they are not a long-term investment strategy.

- Investor-to-investor. Purchases from other large institutional investors that owned the home at enactment or bought it in compliance with the Act.

The law does not push institutional capital out of housing. It pushes it away from buying existing homes off the resale market and toward building new ones. That is the actual policy intent, and it is why the sector reaction has been measured.

Where it could touch STR investors

There is one genuine second-order effect worth stating carefully because the actual version is smaller than the version you will read elsewhere.

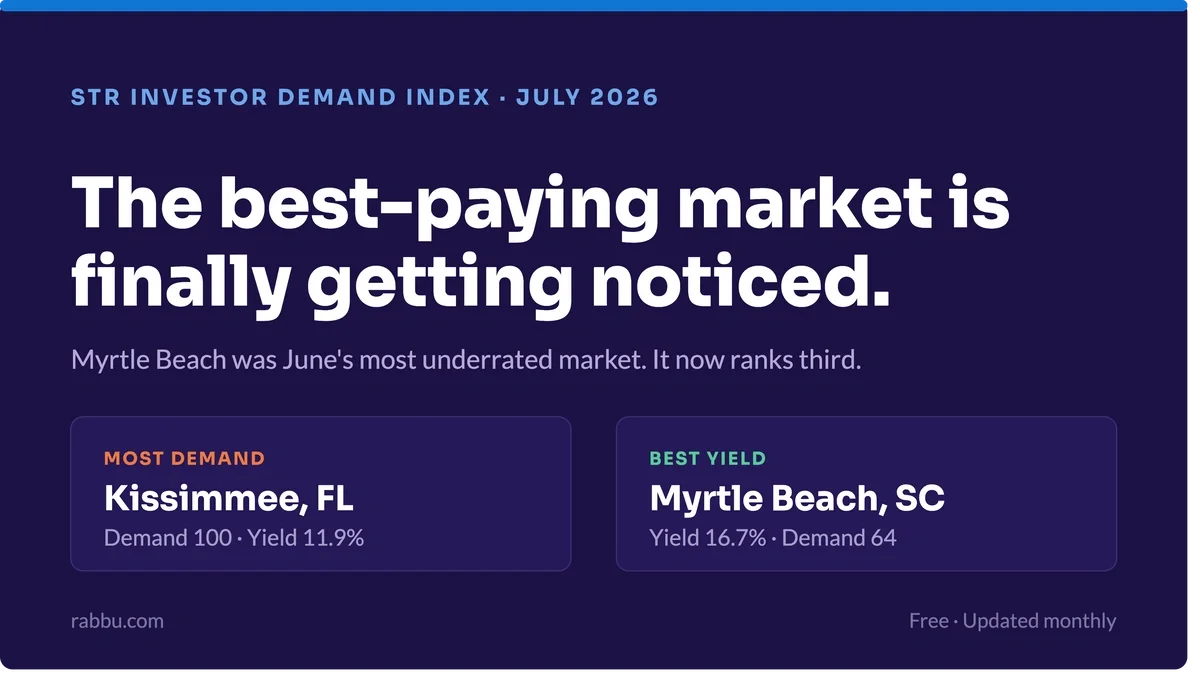

Starting in January 2027, institutional buyers will lose the ability to bid on existing single-family homes. In markets where institutional single-family rental ownership overlaps with short-term rental viable inventory, that removes a competing bidder. The overlap is real but narrow. Institutional single-family rental concentration sits in metros like Atlanta, Phoenix, Dallas, Charlotte, Tampa, and Jacksonville. Most of those are not primary STR investment markets. The clearest exception is the Orlando ring, where institutional long-term rental activity and short-term rental demand genuinely share the same inventory in places like Kissimmee and Davenport.

Whether that translates into better entry pricing for STR buyers in those specific submarkets is an empirical question. It has not happened yet, because the restriction is not in force yet. Anyone telling you today what it will do to Orlando prices is guessing.

We would rather measure it than guess. The STR Investor Demand Index tracks investor demand and delivered median gross yield across U.S. markets on a monthly cadence, using first-party search and lead behavior from investors actually shopping for short-term rentals. If the institutional restriction moves anything in the Orlando cluster, it will show up in the Index in the first half of 2027, and we will publish what we find, whether it confirms this or contradicts it. Until then, it stays on the watch list, not in the conclusion.

The one group that should read the definition twice

If you invest in short-term rentals through a fractional ownership platform, a syndication, or a sponsored fund, the analysis is different from the one above.

The scale test aggregates. It counts homes under investment control "alone or in concert with one or more other entities, directly or indirectly." A sponsor operating dozens of separate special-purpose entities across a vacation-home portfolio does not obviously get to count each entity separately. If that sponsor crosses 350 homes in aggregate, the platform itself may be a covered entity even though no individual investor in it is anywhere close.

This is unresolved. HUD has the authority to issue implementing regulations, including regulations aimed at minimizing market disruption, and how the agency draws the aggregation line will be decided by it. If your STR exposure runs through a sponsor rather than a deed in your own name, ask the sponsor how they read Section 1001 and what their HUD filing position is. Get the answer before January.

What else is in the bill for you

The institutional section is one of twelve titles. Most of the rest is supply-side and long-horizon, but a few pieces touch investors directly.

| Provision | What it does | Relevance to STR buyers |

|---|---|---|

| FHA small-dollar mortgage pilot (Sec. 105) | Authorizes a HUD pilot expanding access to FHA-backed mortgages under $100,000, sunsetting after four years | Low. Below the price band where most STR product pencils, and FHA requires owner occupancy |

| Manufactured housing chassis repeal (Sec. 301) | Eliminates the permanent chassis requirement and sets HUD as the primary authority on energy standards | Watch. It makes factory-built products cheaper to place, but manufactured homes are explicitly carved out of the single-family definition and remain hard to finance and permit as STRs |

| Appraisal reform (Sec. 403, 704) | Expands appraiser training and licensing flexibility, requires value reconsideration procedures on federally backed loans | Modest and positive. More appraiser capacity and a formal path to contest a low value both reduce friction on financed acquisitions |

| NEPA streamlining, zoning frameworks, Innovation Fund, Build Now (Title 2) | Reduces federal review burden and ties some CDBG funding to housing production | Long horizon. New supply reaching your market from these provisions is a 2029 conversation, not a 2027 one |

The bottom line

The corporate homebuying ban does not apply to you unless you control 350 or more single-family homes. It takes effect around January 7, 2027; it is not retroactive, and it forces no one to sell. It contains no short-term rental provisions of any kind, because short-term rental rules are set locally, and this law did not touch them.

The realistic upside is a slightly thinner bidder pool for existing homes in a small number of markets where institutional single-family rental activity overlaps STR-viable inventory, with Orlando the clearest case. That is a hypothesis with a start date, not a reason to change a buy box today.

The things that determine whether a short-term rental works are the same things they were on July 10. Local demand, local supply growth, the local regulatory environment, what you paid, and how well you operate. This law moved none of them.

Notes on this analysis

Statutory descriptions here reflect the final enacted text of H.R. 6644 as summarized by the Bipartisan Policy Center and by counsel analysis published following enactment. Effective dates are calculated from the July 11, 2026 enactment date and are approximate. HUD retains authority to issue implementing regulations that may clarify or narrow several definitions described above, including investment control and aggregation.

This article is general information about federal legislation and is not legal or tax advice. Section 1001 carries civil penalties of up to $1 million per violation. If you believe you may be near the covered threshold, whether directly or through a sponsor, consult counsel before transacting.

Market demand and yield figures referenced from the STR Investor Demand Index follow the published Demand Index methodology. Investor demand and median gross yield are reported as separate measures and are never blended into a single score.