Most short-term rental investors hit the same wall.

The property makes sense. Rabbu's data confirms strong projected revenue. The market is solid. The numbers work — until the financing arrives and quietly changes the math.

Traditional lenders either ignore your Airbnb income entirely or force you to put 20–25% down regardless of how well the property performs. Either way, you end up with less capital, lower returns, and a deal that looks very different on paper than it did when you found it.

That is the problem Rabbu and Total Quality Lending built this partnership to solve.

The Financing Gap for STR Investors

Here is where most lenders fall short for short-term rental investors.

They don't recognize STR income. A property generating $5,000 per month on Airbnb gets underwritten at $2,200 — the long-term rent from the appraisal — because that is all conventional guidelines allow. The income that attracted you to the property does not count.

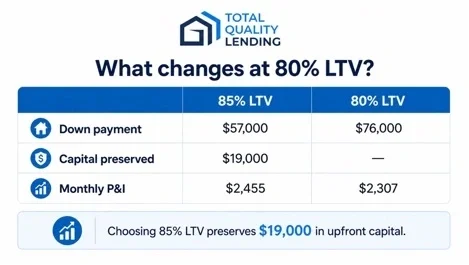

They cap leverage at 75–80% LTV. On a $380,000 purchase, that means $76,000 down minimum. For an investor trying to scale, that is a significant amount of capital locked into a single deal when it could be working in your next acquisition.

TQL's Investor Hybrid Program was built to address both problems directly.

Find a Lender that Specializes in Short-Term Rentals

Connect with lenders who actually understand short-term rental cash flow and offer DSCR loans, portfolio financing, and investor-friendly terms.

Get Matched with STR LendersHow the Investor Hybrid Program Works

The Investor Hybrid Program is a loan product built specifically for short-term rental investors. Two things make it different from everything else on the market.

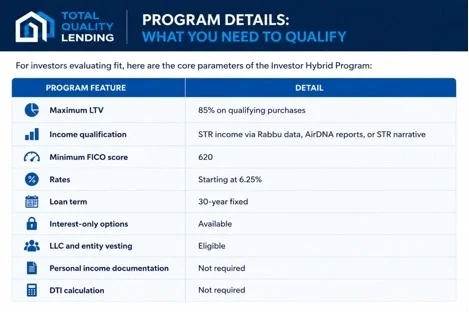

First, it recognizes your actual STR income. Projected revenue supported by Rabbu market data, AirDNA Rentalizer Reports, or an STR income narrative can be used for loan qualification. The income you are buying the property for is the income the lender recognizes — not a long-term appraisal figure that undervalues what the property actually earns.

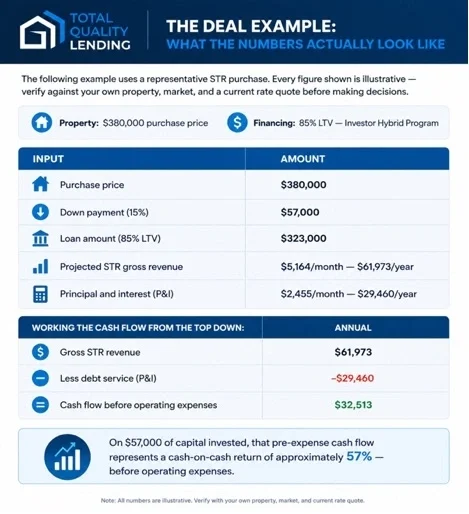

Second, it goes up to 85% LTV on qualifying purchases, meaning as little as 15% down. That extra 5% of preserved capital changes the return profile of every deal you do.

On $57,000 of capital invested, the pre-expense cash flow represents a cash-on-cash return of approximately 57% before operating expenses.

That qualifier matters. STR operating costs — management fees, cleaning, insurance, property taxes, maintenance, and vacancy typically run 30–50% of gross revenue. Your actual net return will be lower. Always model your real operating numbers before making any decision.

What the example demonstrates is the structural advantage: STR income recognized by the lender, financed at 85% LTV, more capital preserved per deal, better return on every dollar invested. That structural improvement is real — and it does not require ignoring expenses to be meaningful.

How Rabbu Fits In

Finding the right STR property is where most investors spend the most time and make the most consequential decisions.

Rabbu is the Airbnb marketplace built specifically for real estate investors. Trusted by 120,000+ investors nationwide, Rabbu lets you browse active Airbnbs for sale with documented historical income, analyze STR-ready homes with live market revenue projections, and connect with specialized agents who have helped investors acquire over $650 million in short-term rental properties.

The income data Rabbu provides is the same data that supports STR income qualification under TQL's Investor Hybrid Program. That means the number you used to evaluate the deal is the number the lender uses to qualify it. The analysis and the financing are finally speaking the same language.

Rabbu finds the deal. TQL finances it — the right way.

Who This Is Built For

The Investor Hybrid Program works best for investors who are:

- Purchasing a property specifically to operate as an Airbnb or vacation rental

- Looking to preserve capital between acquisitions and scale their STR portfolio

- Self-employed or unable to qualify through conventional income documentation

- Holding or planning to hold investment properties in an LLC

- Using Rabbu income data to evaluate and underwrite deals before financing

It is a less ideal fit if your target market has weak or uncertain STR demand, if local STR regulations are unclear or tightening, or if you are not comfortable carrying a larger loan balance. Higher leverage improves returns when the property performs and increases exposure when it does not. Underwrite your deals honestly.

The Bottom Line

STR income recognized. 85% LTV. No personal income documentation required. No DTI calculation.

Those four things rarely exist in the same loan product. The Investor Hybrid Program brings them together — and Rabbu's income data connects directly to how TQL qualifies your deal.

If you are evaluating a short-term rental and want to understand what the financing actually looks like on your specific property, we are happy to run through it with you.

Browse Airbnbs for sale and analyze your deal at rabbu.com.

Submit an STR scenario or schedule a strategy call at tqltpo.totalqualitylending.com.

Frequently Asked Questions

What is the minimum down payment for the Investor Hybrid Program?

Qualifying borrowers can put as little as 15% down — compared to the 20–25% required by most standard investment property loan programs. On a $380,000 purchase, that means $57,000 down instead of $76,000, preserving approximately $19,000 for reserves, renovation, or your next acquisition.

Can Airbnb or short-term rental income be used to qualify for this loan?

Yes. The Investor Hybrid Program accepts projected STR income supported by Rabbu market data, AirDNA Rentalizer Reports, or an STR income narrative. Personal income documentation is not required. Qualification is based on the property's projected rental income rather than the borrower's personal tax returns or W-2s.

Can I hold the property in an LLC?

Yes. LLC and entity vesting is eligible under the Investor Hybrid Program. This is not permitted under conventional Fannie Mae and Freddie Mac guidelines, making LLC eligibility one of the significant practical advantages of this program for investors who want liability protection and organizational clarity across their portfolio.

What credit score is required?

The minimum FICO score is 620. Higher credit scores generally support better rates and more favorable terms.

How does Rabbu's income data support loan qualification?

Rabbu provides STR-ready homes with revenue projections modeled from live market data that is continuously updated. That data — the same information investors use to evaluate a deal before buying — can be used to support income qualification under TQL's Investor Hybrid Program, allowing the property's actual short-term rental income potential to factor into the financing rather than being replaced by a lower long-term rent appraisal figure.

How do I get started?

Browse Airbnbs for sale and run your deal analysis at rabbu.com. To talk financing, visit tqltpo.totalqualitylending.com to submit a scenario or schedule a strategy call with TQL's team.

Total Quality Financial, Inc. | NMLS #1933377. This article is intended for informational and educational purposes only and is not a commitment to lend or extend credit. Loan products, rates, terms, qualification requirements, and availability are subject to change without notice and underwriting approval. Not all applicants will qualify. Cash-on-cash figures shown are illustrative examples and do not include operating expenses — actual returns vary by property, market, operating costs, and financing terms. Equal Housing Lender. For licensing information, visit www.nmlsconsumeraccess.org.

Rabbu, Inc. is an independent third-party marketplace platform. Rabbu is not a lender and does not provide financing. Revenue projections provided by Rabbu are market-modeled estimates and are not guarantees of future performance. Investors should conduct their own due diligence before making any investment decision.