For the first time since 2022, average 30-year mortgage rates have fallen below 6%, landing around 5.9% according to Freddie Mac data. This milestone has grabbed headlines because it represents the most attractive borrowing environment real estate investors have seen in years.

But what does this really mean for STR (short-term rental) investors? And more importantly, how should it influence the way you underwrite deals in 2026?

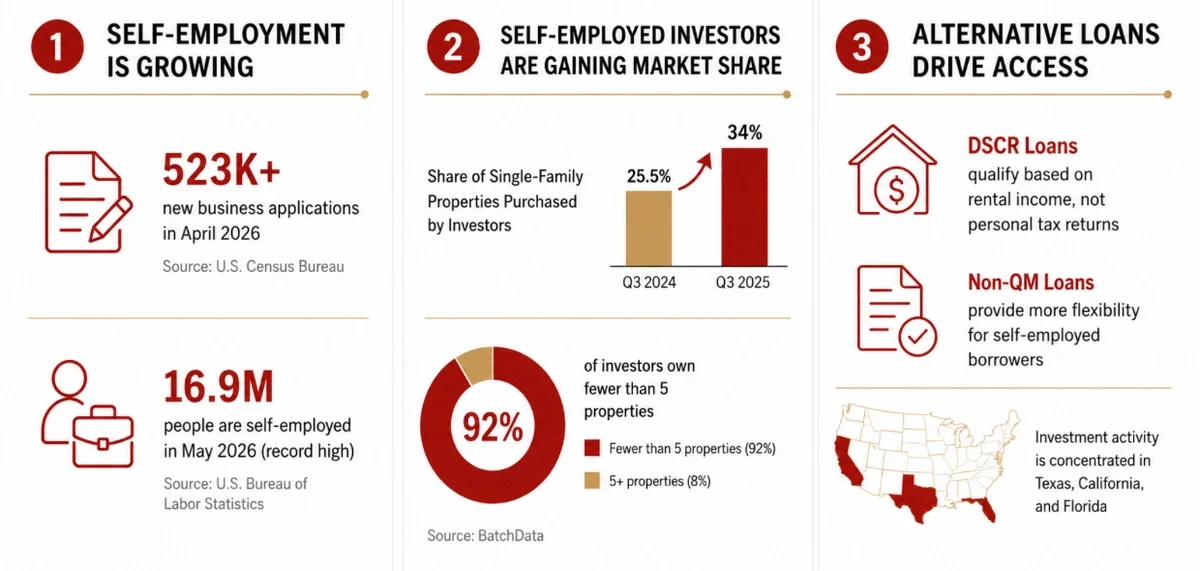

Here’s a breakdown of what’s changing and why it matters.

Lower Rates Boost Buying Power

When mortgage rates fall, everything else equal, your monthly payment goes down. That improves:

- Cash flow projections

- Debt service coverage

- Purchase price flexibility

For example, a 30-year loan at 5.9% will have a significantly lower monthly payment than the same loan at 6.7% or higher, which was common a year ago. This creates real breathing room for underwriting without sacrificing leverage.

For STR investors this matters because financing has been one of the biggest headwinds in recent years. Lower rates can make more deals pencil on cash flow rather than on pure appreciation or just tax savings.

Competition May Heat Up

Lower rates often bring more buyers into the market because financing becomes more affordable. That can lead to:

- More competition for properties

- Higher purchase prices

- Stronger negotiation environments

Even though rates are below 6%, home prices remain elevated compared with historical norms. That means buyers still need discipline — falling rates don’t automatically create bargains.

For STR investors this is a critical distinction: better financing doesn’t always mean better deals if pricing rises faster than underwriting reality.

Refinancing and Portfolio Strategy

Lower rates also create refinancing opportunities for owners who bought during periods of high borrowing costs. STR investors who locked in rates above 7% can now consider:

- refinancing to improve cash flow

- pulling equity for additional acquisitions

- restructuring debt to match seasonality or revenue patterns

This dynamic introduces a flexibility that has been absent in the 6%+ rate environment. Sound underwriting should now include both purchase and refinance scenarios to quantify optionality.

Lower Rates Don’t Solve Liquidity Problems

One big constraint that has kept many potential buyers sidelined is what economists call “rate-lock” — homeowners with ultra-low mortgage rates from earlier cycles are reluctant to move because they’d have to give up their cheap financing. That has kept inventory tight and limited supply in many markets.

For STR investors this is a double-edged sword:

- Good: Less new inventory can slow downward pressure on nightly rates.

- Bad: Fewer homes for sale means limited deal flow unless you compete aggressively.

STR success in 2026 will hinge less on broad affordability headlines and more on your ability to identify motivated sellers and structure deals where financing advantages overcome price competition.

What This Means for STR Underwriting

Here’s how lower rates should change your approach:

- Update your debt service models

- Lower rates directly improve cash flow scenarios and debt service ratios.

- Run purchase vs refinance cases

- Especially for existing owners with high rate debt — quantify the impact.

- Continue to demand underwriting discipline

- Even with lower financing costs, overpaying erodes ROI.

-

Identify markets where liquidity responds

- Not all markets will see increased supply just because rates are lower.

Bottom Line

Mortgage rates below 6% are good news for STR investors, but they are not a silver bullet.

They lower borrowing costs and improve financial flexibility, but they do not automatically produce better deals if competition pushes prices higher or inventory remains tight.

If you want help identifying markets where lower rates create the best acquisition opportunities and connecting with agent partners who understand STR nuances, explore top performing areas and get connected through Rabbu.

What STR Investors Should Track Next

As you think about purchases in 2026, keep a close eye on:

- Inventory changes as buyers reenter the market

- Refinancing activity and its impact on supply

- Market pricing relative to cash flow assumptions

Mortgage rates are one piece of the puzzle. The rest still comes down to fundamentals, competitive dynamics, and execution.